MOOC List is learner-supported. When you buy through links on our site, we may earn an affiliate commission.

MOOC List is learner-supported. When you buy through links on our site, we may earn an affiliate commission.

This course is an introduction to stochastic processes through numerical simulations, with a focus on the proper data analysis needed to interpret the results. We will use the Jupyter (iPython) notebook as our programming environment. It is freely available for Windows, Mac, and Linux through the Anaconda Python Distribution.

The students will first learn the basic theories of stochastic processes. Then, they will use these theories to develop their own python codes to perform numerical simulations of small particles diffusing in a fluid. Finally, they will analyze the simulation data according to the theories presented at the beginning of course.

At the end of the course, we will analyze the dynamical data of more complicated systems, such as financial markets or meteorological data, using the basic theory of stochastic processes.

What you'll learn

- Basic Python programming

- Basic theories of stochastic processes

- Simulation methods for a Brownian particle

- Application: analysis of financial data

Syllabus

Week 1: Python programming for beginners

- Using Python, iPython, and Jupyter notebook

- Making graphs with matplotlib

- The Euler method for numerical integration

- Simulating a damped harmonic oscillator

Week 2: Distribution function and random number

- Stochastic variable and distribution functions

- Generating random numbers with Gaussian/binomial/Poisson distributions

- The central limiting theorem

- Random walk

Week 3: Brownian motion 1: basic theories

- Basic knowledge of Stochastic process

- Brownian motion and the Langevin equation

- The linear response theory and the Green-Kubo formula

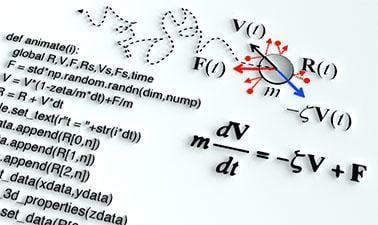

Week 4: Brownian motion 2: computer simulation

- Random force in the Langevin equation

- Simple Python code to simulate Brownian motion

- Simulations with on-the-fly animation

Week 5: Brownian motion 3: data analyses

- Distribution and time correlation

- Mean square displacement and diffusion constant

- Interacting Brownian particles

Week 6: Stochastic processes in the real world

- Time variations and distributions of real world processes

- A Stochastic Dealer Model I

- A Stochastic Dealer Model II

- A Stochastic Dealer Model III

MOOC List is learner-supported. When you buy through links on our site, we may earn an affiliate commission.

MOOC List is learner-supported. When you buy through links on our site, we may earn an affiliate commission.